Why lender fit, structure, and positioning matter more than how many doors you knock on.

One of the biggest misconceptions I see is that if you talk to enough lenders, eventually one of them will say yes.

It feels logical. More shots on goal, better odds. In practice, it usually works the opposite way.

Most deals don’t fall apart because nobody had capital. They fall apart because the deal was shown to the wrong part of the market, in the wrong way, at the wrong time. And once that happens, it’s hard to unwind the damage. The same dynamic shows up in real estate and in capital markets just as much as it does in operating company financings.

When I’m speaking with a CFO or an owner, the first thing I usually say is: this is not about access. Access is easy. Anyone can send your deck to fifty lenders. What matters is fit. And fit is what determines whether a credit committee can actually get comfortable and approve something.

Behind every “lender” is a credit committee. Not the relationship manager you’re talking to. Not the business development person who likes the story. A small group of risk people who have to defend the loan internally, to their board, to regulators, and to their own careers. Their job is not to be creative. Their job is to not make a mistake.

So the question is never “is this a good business?”

The question is “does this deal, structured this way, fit our box right now, and can we justify it if something goes wrong?”

That’s a very different lens than most borrowers are using when they start a financing process.

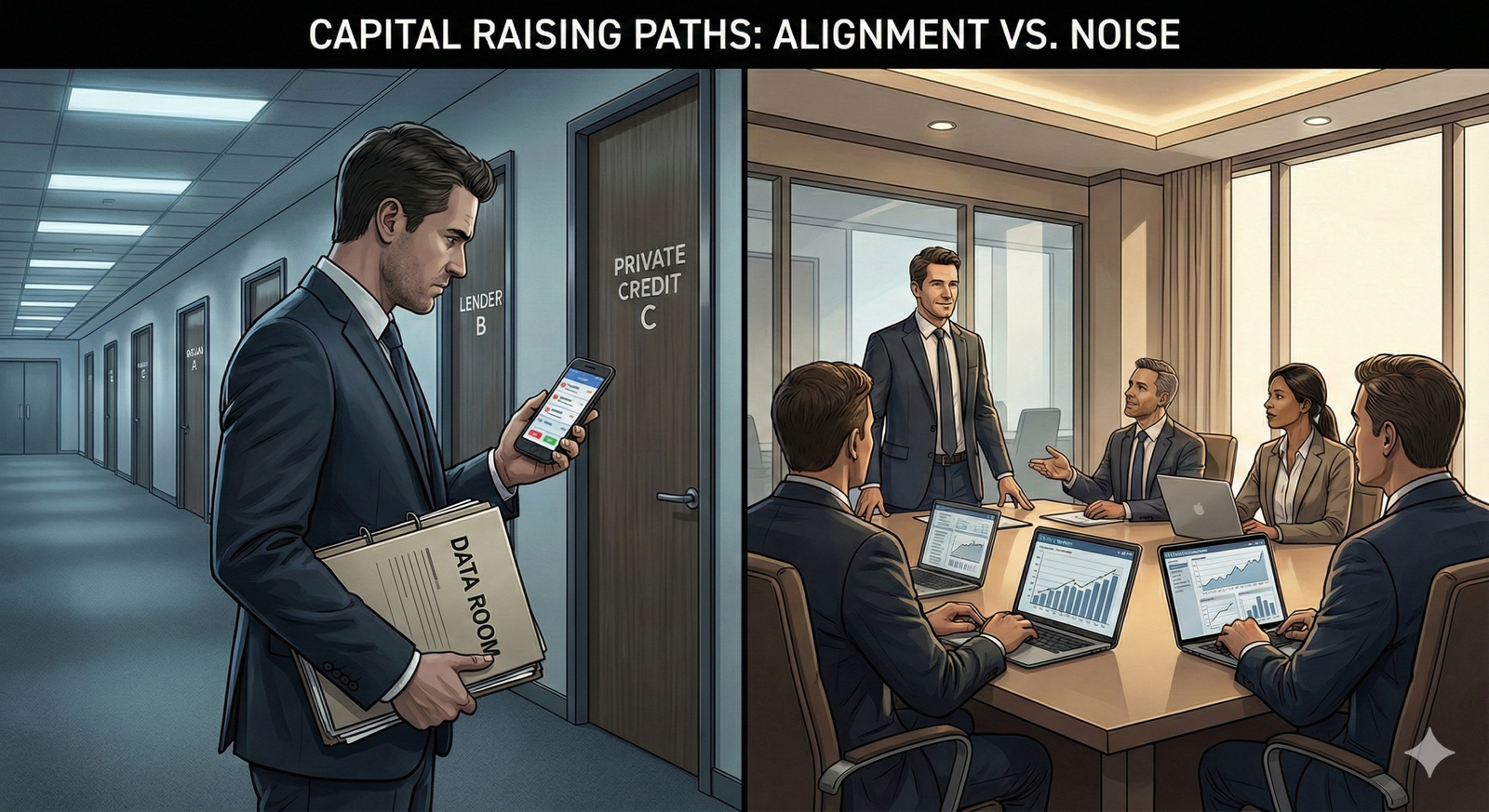

A common situation looks like this: a company needs, say, $8 million for growth or an acquisition. They start with their bank. The bank likes them, but leverage is a little high, collateral is a little thin, or the use of funds is a little outside policy. So the bank tries to make it work. Credit pushes back. Terms change. Advance rates come down. Covenants get tighter. Maybe a personal guarantee shows up. Eventually the structure no longer matches what the company was trying to accomplish.

Then the company goes to another lender. And another. Each one looks at it through a slightly different box, but the process is still reactive. The structure is being shaped by whoever happens to be in front of you at the moment.

Meanwhile, the deal is quietly getting “shopped.” Lenders talk. Credit people see repeat opportunities. And even if no one is saying anything improper, the optics shift. Instead of “new, well-positioned opportunity,” the deal starts to feel like “this has been around and hasn’t found a home yet.” Nobody wants to be the one catching a falling knife, and that alone changes how cautiously it’s underwritten.

This is where we spend most of our time with clients: before a single lender is called.

We try to understand, very plainly, what the real constraints are. Cash flow under stress, collateral reality, timeline, exit, how much flexibility there is on structure, and what the business can actually live with if the market pushes back. Not what would be nice. What is realistic.

Sometimes that means saying: this won’t clear a senior bank box, even if you have a great relationship. Or: this is bridge capital, not term capital, even if the pricing looks uncomfortable. Or: this is going to require a private credit solution, not because banks are bad, but because the structure you need doesn’t match how banks are allowed to lend.

Once you get honest about that, the process changes. You stop thinking in terms of “who do we know at which bank” and start thinking in terms of “which segment of the market is actually built to underwrite this risk, this structure, and this timeline.”

That’s also why we’re very careful about how many lenders we engage. It’s not about creating a beauty contest. It’s about protecting the borrower’s credibility and the lender’s time. A tight, well-targeted group of lenders who truly fit the deal almost always produces a better outcome than a wide process that creates noise, mixed signals, and fatigue.

From the lender side, that discipline matters too. Good lenders don’t want to see deals that have been broadly circulated with no clear positioning. They want to see opportunities that were thought through, structured intentionally, and brought to them for a reason.

So when we talk about probability of close, we’re not talking about hustle. We’re talking about design.

Designing the structure before the outreach.

Designing the narrative before the data room.

Designing the lender list before the process starts.

And being very straightforward with the client about what the market is likely to say, what it’s unlikely to say, and where the real friction points will be. Not to discourage a transaction, but to make sure nobody is surprised three months later when credit committee focuses on exactly the things that could have been anticipated on day one.

We’re not decision-makers for lenders, and we can’t change credit policy. What we can do is help make sure a deal walks into the right room, with the right structure, and the right expectations, instead of trying every door in the building and hoping one opens.

That, more than access, is what actually determines whether a capital raise closes.